By: Paul G. Barden, Esq. | Settlement Strategist, Paramount Settlement Planning

As a trial attorney for 26 years, I had several occasions to structure my senior client’s settlements. However, I assumed that for clients in their mid-fifties and beyond, structures were not an appropriate settlement vehicle. Four months into my transition as a Settlement Strategist with Paramount Settlement Planning, I realize how short-sighted I was in not considering a structure for even my most senior clients.

Take a look at the important strategies set forth below and you will likely change your opinion about “structuring for seniors.”

I. INCOME STREAMS THE SENIOR PLAINTIFF CAN NOT OUTLIVE

Numerous surveys cite Americans’ greatest fear in retirement is running out of money. According to the National Center for Health Statistics, the average American can expect to live nearly 80 years, and by the time they reach their 50’s, the life expectancy rises into the mid-80s.

There are other studies that show that most personal injury claimants (and lottery winners), regardless of the size of the payout, squander their proceeds in a relatively short period of time. Many end up broke and bankrupt.

Structured settlements provide guaranteed, stable income for the rest of the client’s life. Importantly, guarantee periods are frequently used to protect the income for surviving spouses.

Structures protect clients from themselves – avoiding the temptation of living beyond their means by spending large sums of money on lavish vacations, homes, or cars.

Structures protect the client from predators – family, friends, and unscrupulous investment firms.

Structures avoid the volatility and uncertainties of other market investment options.

For the client who was working prior to their injury, a structure can replace income if the client is no longer capable of working.

II. SOCIAL SECURITY RETIREMENT MAXIMIZATION STRATEGY

A structure may also provide sufficient monthly income to a client in their 60’s, allowing them to defer taking any social security benefits at the earliest possible age of 62 (which would be at a 25% reduction), at the full retirement age of 66 or 67, and deferring all the way to age 70 where they could realize 25% more each month.

III. ESCAPE FROM PROBATE

Some clients may be secure in their own retirement and are looking to pass along the proceeds of their settlement to their children and grandchildren. Should the client take a lump sum cash payout at the time of settlement, any settlement funds still held by the client at the time of their death becomes a part of the estate and passes through the probate process. However, if the client was receiving annuity payments at the time of their death (or the death of the client and the spouse if a joint life product), the remainder of those funds will pass to the client’s named beneficiaries outside of probate.

IV. THE PLAINTIFF “LEGACY” PLAN

Suppose the plaintiff, 73-year-old James Smith, will net $500,000.00 from his $800,000.00 settlement. He has three grandchildren who are the targets of his affection and who he wants to make sure can afford the college of their choice without them going deeply into debt.

James initially thought about putting $40,000.00 for each child in an account for them to use towards college; a 529 plan or some similar investment account. However, James recently ran into a friend at the barbershop who informed him that he had set up similar plans for his grandchildren in the amount of $10,000.00 per child. Regrettably, he found out that the funds in these accounts would minimize eligibility for any need-based financial aid programs until those accounts were spent down. Further, with 529 plans, the gifted amount must be used to pay for high school, college, or other qualifying higher education costs, otherwise, they could face adverse tax consequences.

It was almost as if the plan cost the children potential benefits and the money was wasted.

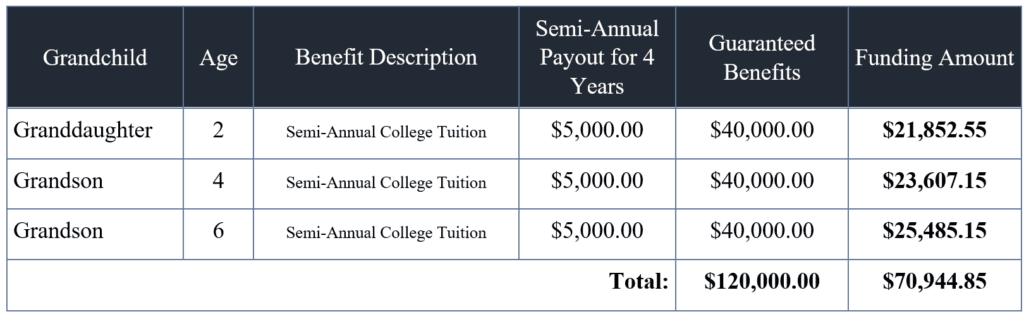

James then met with his personal injury attorney and settlement planner who advised him that instead of taking $120,000.00 in cash and setting it aside for the grandchildren he could elect to structure $71,000.00 of his settlement to provide the same $120,000.00 in benefits to assist in his grandchildren’s college education (see structured settlement illustration in figure 1).

More importantly, with a structured settlement, he would be able to select the timing of the distribution, setting the payments up for dates after the college financial aid applications were due.

While the payments would come in semiannually, they would be payable, tax-free, to James and he could distribute them appropriately. Additionally, in the event of James’ death, by virtue of the beneficiary designations in the structured settlement contracts, those payments would go to his grandchildren directly at the designated semi-annual times.

This is such an important tool for providing a legacy from James to his grandchildren that he’s thinking about doubling his contribution to this portion of the structured settlement funding amount which would have the same impact on their benefits.

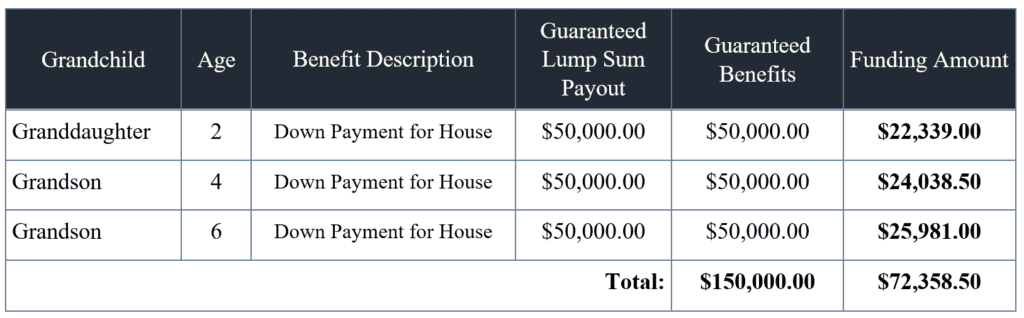

Impressed by the structured settlement’s ability to provide legacy benefits at a deep discount, James is also considering keeping the college contributions the same and creating a guaranteed tax-free down payment on a home of $50,000.00 for each of the grandchildren at the age of 25. This additional benefit cost only $26,000.00 for his oldest grandson and just over $22,000.00 for his granddaughter. (see structured settlement illustration in figure 2).

V. QUALIFIED RETIREMENT DRAWDOWN SUBSTITUTION STRATEGY (TAX SAVINGS PLAN)

As it turns out James has significant assets in his own retirement account and is living off of the withdrawals from those qualified savings. However, every dollar that he takes out from his qualified account is taxed at the ordinary income tax rates both at the federal and state levels. That combined tax rate is approximately 29%.

He questions whether or not a structured settlement might help him reduce his tax burden and allow his qualified retirement assets to continue to grow. Rather than taking $180,000.00 of the remaining proceeds in a lump sum of cash, statistically shown to be whittled away before he turns 75, Mr. Smith can fund a structured settlement with $180,000.00 of the remaining funds, yielding approximately $1,020.00 per month, over the next twenty years.

This proposal would guarantee Mr. Smith $244,495.00 in total benefits paid out over those twenty years. This equates to a taxable equivalent yield of 4.47% based on a marginal combined tax rate of 29%. He could then stop taking $12,000.00 per year from his retirement savings and live off of the tax-free structured benefit allowing himself to save $3,500.00 in combined taxes each year ($70,000.00 over 20 years of the guaranteed payment stream should Mr. Smith live that long).

Those savings would continue to grow for his survivor or the next generation.

VI. ASSET (NURSING HOME EVAPORATION) PROTECTION

As mentioned, Mr. Smith has accumulated significant retirement savings and other savings. He is fearful that if he must go into a nursing home, all of those funds might be forced to be used to pay for the nursing home. At his age, long-term care insurance is very expensive. However, this must be weighed against the possibility of the depletion of his entire estate to pay for nursing home care. Mr. Smith has researched prices for nursing home costs as well as quotes for long-term care insurance.

In this scenario, Mr. Smith would use $1,020.00 in a monthly payout benefit from a structured settlement to cover the [monthly] premium cost of a bundled long-term care plan providing benefits of $14,000.00 per month ($168,000.00 per year), and which has inflation protection built-in at 3%. Using the structured settlement to fund the costs of long-term care insurance ensures that he will always be able to make the premium payment for his long-term care insurance.

CONCLUSION

If you’re a personal injury practitioner, don’t sell your senior clients short.

Paramount Settlement Planning is dedicated to preserving the greatest benefits and quality of life for plaintiffs following their settlement and protecting the settlement funds from dissipation. When considering whether or not a structured settlement might be right for your client or yourself in the form of a tax-deferred attorney fee structure, it is imperative that you have your own representative in your corner, advocating for the plaintiff and your firm. Since 2003, Paramount Settlement Planning and its experienced attorneys and settlement planners only represent plaintiffs and their counsel in structured settlement transactions.